The big, rarely asked question about our current economy is who gets the benefits of common wealth? Common wealth has several components. One consists of gifts of nature we inherit together: our atmosphere and oceans, watersheds and wetlands, forests and fertile plains, and so on (including, of course, fossil fuels). In almost all cases, we overuse these gifts because there’s no cost attached to using them.

Another component is wealth created by our ancestors: sciences and technologies, legal and political systems, our financial infrastructure, and much more. These confer enormous benefits on all of us, but a small minority reaps far more financial gain from them than most of us do.

Yet another chunk of common wealth is what might be called “wealth of the whole”?—?the value added by the scale and synergies of our economy itself. The notion of “wealth of the whole” dates back to Adam Smith’s insight that labor specialization and the exchange of goods?—?pervasive features of a whole system?—?are what make nations rich. Beyond that, it’s obvious that no business can prosper by itself: all businesses need customers, suppliers, distributors, highways, money and a web of complementary products (cars need fuel, software needs hardware, and so forth). So the economy as a whole is not only greater than the sum of its parts, it’s an asset without which the parts would have almost no value at all.

The sum of wealth created by nature, our ancestors and our economy as a whole is what I here call common wealth. Several things can be said about our common wealth. First, it’s the goose that lays almost all the eggs of private wealth. Second, it’s extremely large but mostly invisible. Third, because it’s not created by any individual or business, it belongs to all of us jointly. And fourth, because no one has a greater claim to it than anyone else, it belongs to all of us equally.

The big, rarely asked question about our current economy is who gets the benefits of common wealth? No one disputes that private wealth creators are entitled to the wealth they create, but who is entitled to the wealth we share is an entirely different question. My contention is that the rich are rich not because they create a large amount of wealth, but because they capture a larger share of common wealth than they’re entitled to. Another way to say this is that the rich are as rich as they are?—?and the rest of us are poorer than we should be?—?because extracted rent far exceeds virtuous rent. If that’s the case, the appropriate remedy is to diminish the first kind of rent and increase the second kind.

A perfect example of virtuous rent is the money paid to Alaskans by the Alaska Permanent Fund. Since 1980, the Permanent Fund has distributed equal yearly dividends to every person who resides in Alaska for one year or more. The dividends?—?which have ranged from $1,000 to $3,269 per person?—?come from a giant mutual fund whose beneficiaries are all the people of Alaska, present and future. The fund is capitalized by earnings from Alaska’s oil, a commonly owned resource. Given the steady flow of cash to its entire population, it’s not surprising that Alaska has the highest median income and one of the lowest poverty rates of any state in the nation.

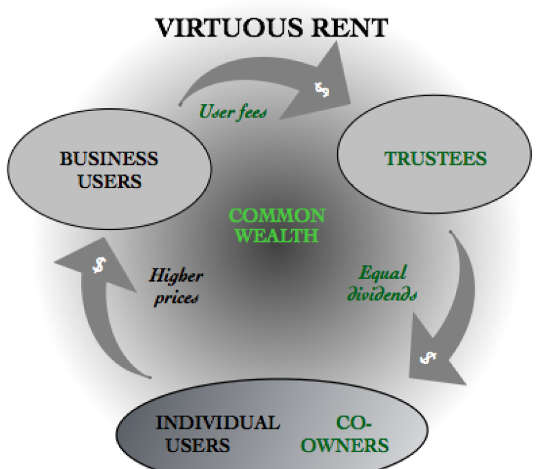

More generically, virtuous rent is any flow of money that starts by raising the cost of harmful or extractive activity and ends by increasing the incomes of all members of society. Another way to think of it is as rent that we, as collective co-owners, charge for private use of our common assets. Think, for example, of charging polluters for using our common atmosphere and then sharing the proceeds equally.

Virtuous rent would be collected by not-for-profit trusts that represent all members of a polity equally. It would be generated by charging private businesses for using common assets that most of the time they use for free. Such rent would also lead to higher prices, but for good reasons: to make businesses pay costs they currently shift to society, nature and future generations, and to offset traditional rent.

Externalities are a better-known concept than common wealth. They’re the costs businesses impose on others?—?workers, communities, nature and future generations?—?but don’t pay themselves. The classic example is pollution.

Almost all economists accept the need to “internalize externalities,” by which they mean making businesses pay the full costs of their activities. What they don’t often discuss are the cash flows that would arise if we actually did this. If businesses pay more money, how much more, and to whom should the checks be made out?

These aren’t trivial questions. In fact, they’re among the most momentous questions we must address in the twenty-first century. The sums involved can, and indeed should, be very large?—?after all, to diminish harms to nature and society, we must internalize as many unpaid costs as possible. But how should we collect the money, and to whom should it go?

One way to collect the money was proposed nearly a century ago by British economist Arthur Pigou, a colleague of Keynes’ at Cambridge. When the price of a piece of nature is too low, Pigou said, government should impose a tax on using it. Such a tax would reduce our usage while raising revenue for government.

In theory Pigou’s idea makes sense; the trouble with it lies in implementation. No Western government wants to get into the business of price-setting; that’s a job best left to markets. And even if politicians tried to adjust prices with taxes, there’s little chance they’d get them “right” from nature’s perspective. Far more likely would be tax rates driven by the very corporations that dominate government and overuse nature now.

An alternative is to bring some non-governmental entities into play; after all, the reason we have externalities in the first place is that no one represents stakeholders harmed by shifted costs. But if those stakeholders were represented by legally accountable agents, that problem could be fixed. The void into which externalities now flow would be filled by trustees of common wealth. And those trustees would charge rent.

As for whose money it is, it follows from the above that payments for most externalities?—?and in particular, for costs imposed on living creatures present and future?—?should flow to all of us together as beneficiaries of common wealth. They certainly shouldn’t flow to the companies that impose the externalities; that would defeat the purpose of internalizing them. But neither should they flow to government, as Pigou suggested.

In my mind, there’s nothing wrong with government taxing our individual shares of common wealth rent, just as it taxes other personal income, but government shouldn’t get first dibs on it. The proper first claimants are we, the people. One could even argue, as economist Dallas Burtraw has, that government capture of this income may be an unconstitutional taking of private property.

There are several further points that can be made about virtuous rent. First, paying virtuous rent to ourselves has a very different effect than paying extractive rent to Wall Street, Microsoft or Saudi princes. In addition to discouraging overuse of nature, it returns the money we pay in higher prices to where it does our families and economy the most good: our own pockets. From there we can spend it on food, housing or anything else we choose.

Such spending not only helps us; it also helps businesses and their employees. It’s like a bottom-up stimulus machine in which the people rather than the government do the spending. This is no trivial virtue at a time when fiscal and monetary policy have both lost their potency.

Second, virtuous rent isn’t a set of government policies that can be changed when political winds shift. Rather, it’s a set of pipes within the market that, once in place, will circulate money indefinitely, thereby sustaining a large middle class and a healthier planet even as politicians and policies come and go.

Notice that there are no taxes or government programs in the above diagram. The money collected is in the form of prices for value received. The money distributed is property income paid to owners.

Lastly, though virtuous rent requires government action to get started, it has the political virtue of avoiding the bigger/smaller government tug-of-war that paralyzes Washington today. It thus can appeal to voters and politicians in the center, left and right.

A trim tab is a tiny flap on a ship or airplane’s rudder. The designer Buckminster Fuller often noted that moving a trim tab slightly turns a ship or a plane dramatically. If we think of our economy as a moving vessel, the same metaphor can be applied to rent. Depending on how much of it is collected and whether it flows to a few or to many, rent can steer an economy toward extreme inequality or a large middle class. It can also guide an economy toward excessive use of nature or a safe level of use. In other words, in addition to being a wedge (as Henry George put it), rent can also be a rudder. An economy’s outcomes depend on how we turn the rudder.

Consider the board game Monopoly. The object is to squeeze so much rent out of other players that you wind up with all their money. You do this by acquiring land monopolies and building hotels on them. However, there’s another feature of the game that offsets this extracting of rent: all players get an equal cash infusion when they pass Go. This can be thought of as virtuous rent.

As Monopoly is designed, the rent extracted through monopoly power greatly exceeds the rent players receive when passing Go. The result is that the game always ends the same way: one player gets all the money. But suppose we tip the scale the other way. Suppose we decrease the extracted rent and increase the virtuous kind. For example, we could pay players five times as much for passing Go and reduce hotel rents by half. What then happens?

Instead of flowing upward and concentrating in the hands of a single winner, rent flows more evenly. Instead of the game ending when one player takes all, the game continues with many players receiving a steady flow of income. The player with the most money can be declared the winner, but she or he doesn’t get everything and other players needn’t go bankrupt.

The point here is that different rent flows can steer a game?—?and more importantly, an economy?—?toward different outcomes. Among the outcomes that can be affected by differing rent flows are the levels of wealth concentration, pollution and real investment as opposed to speculation.

Rent, in other words, is a powerful tool. And it’s also something we can fiddle with. Do we want less extracted rent? More virtuous rent? If so, it’s up to us to build the pipes and turn the valves.

This is an excerpt of a longer article

which originally appeared in OnTheCommons

About The Author

OTC co-founder Peter Barnes is writer and entrepreneur whose work focuse on fixing the deep flaws of capitalism. He has co-founded several socially responsible businesses (including Credo Mobile) and written numerous articles and books, including Capitalism 3.0 and With Liberty and Dividends For All.

Related Books

at InnerSelf Market and Amazon